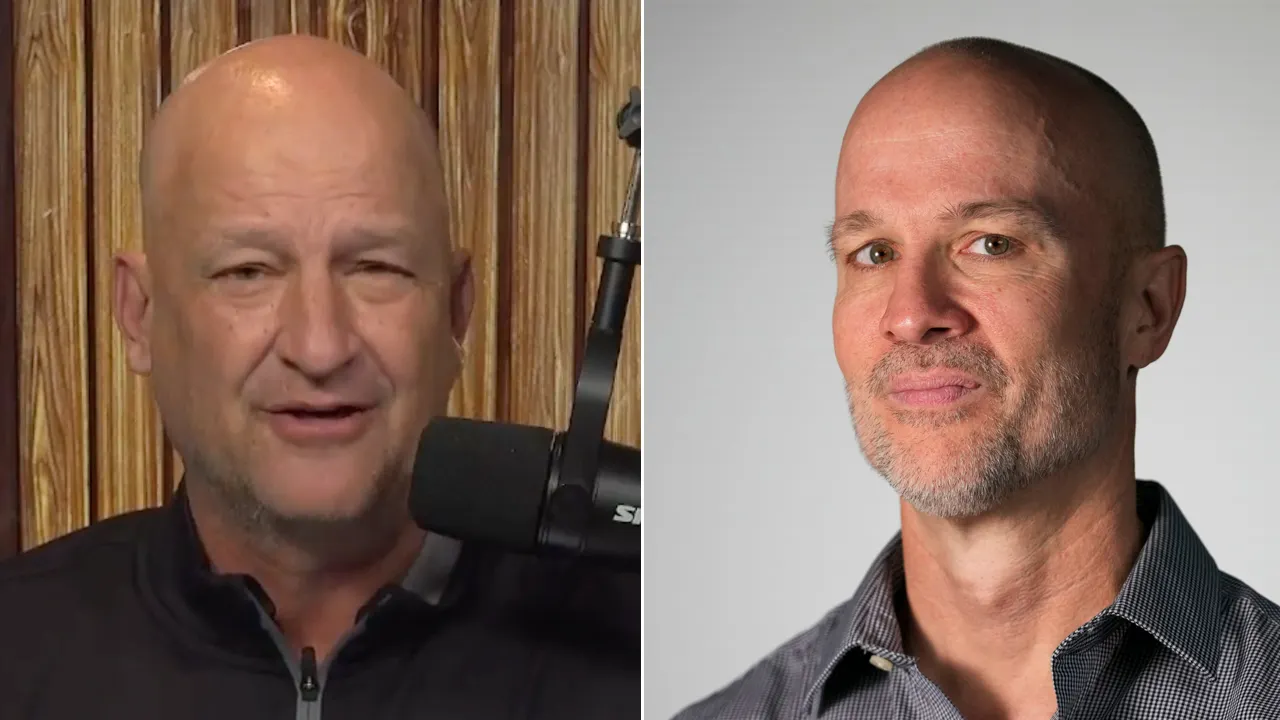

Dan Dakich Slams Columnist Over Bizarre Interaction With Caitlin Clark: 'Why Is It Okay?'

Dan Dakich spoke Thursday about Indy Star columnist Gregg Doyel and the bizarre interaction he had during Caitlin Clark's press …

Dan Dakich spoke Thursday about Indy Star columnist Gregg Doyel and the bizarre interaction he had during Caitlin Clark's press …

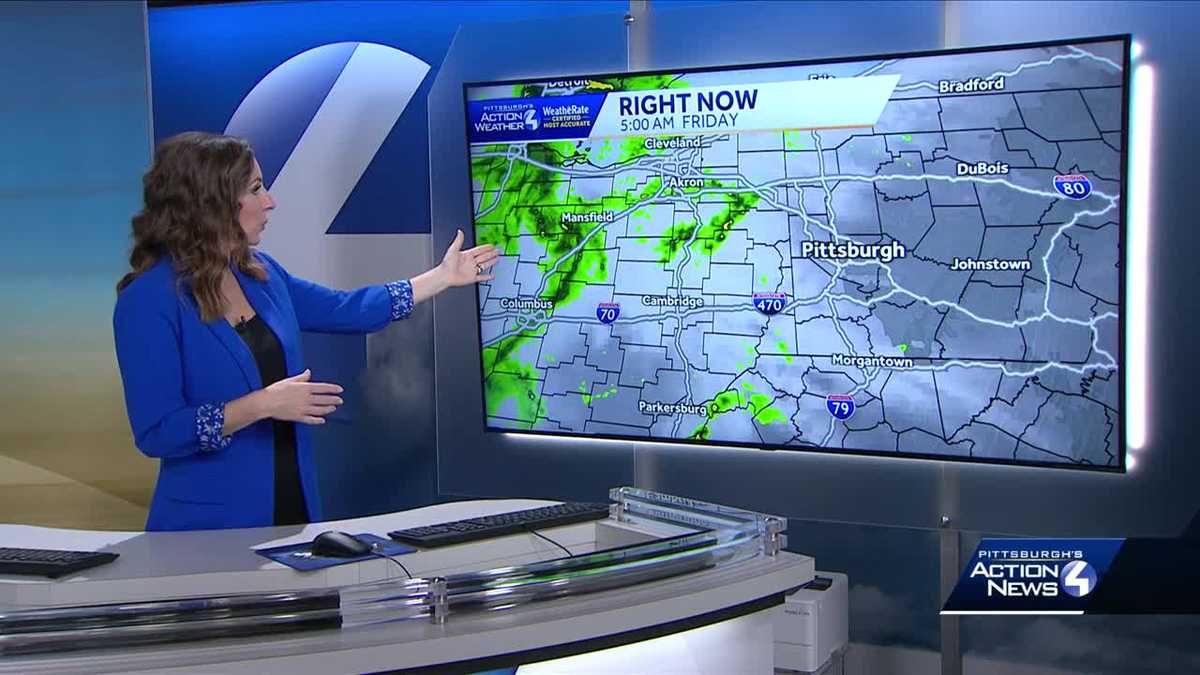

Rain might impact Friday’s morning commute in some parts of the Pittsburgh area Things will dry out later in the …

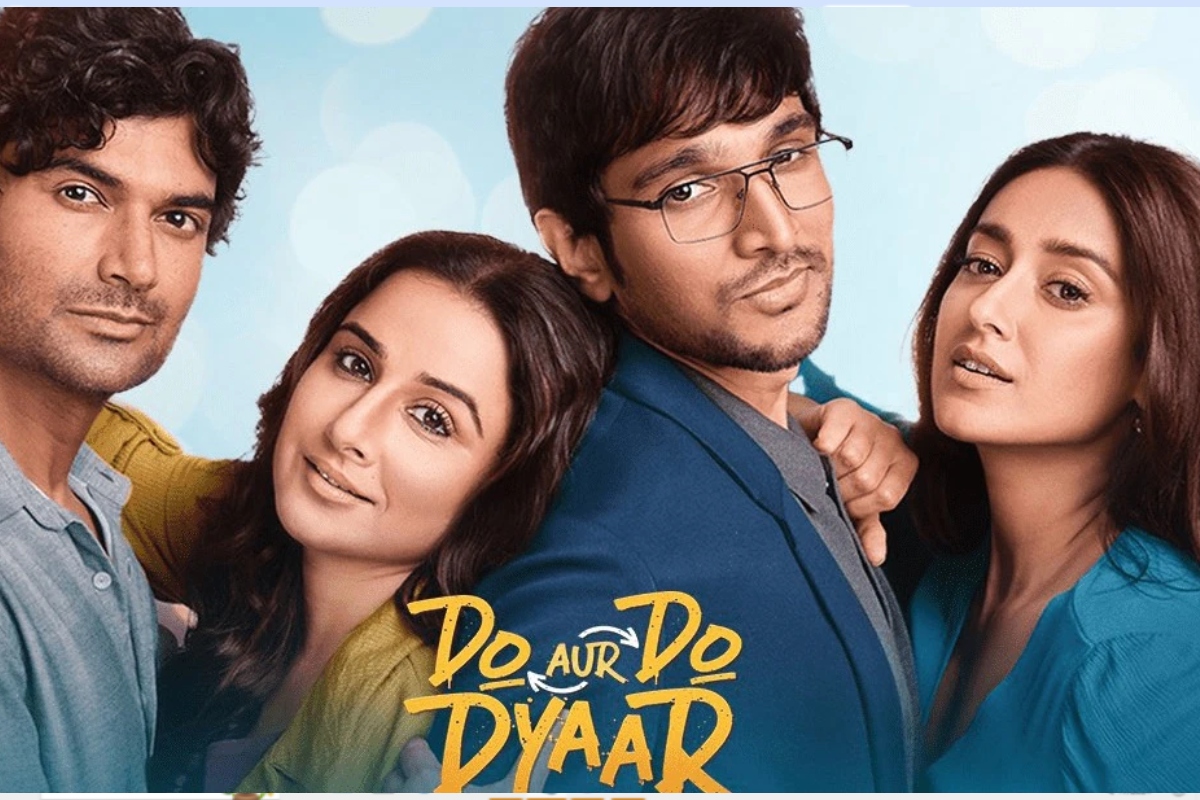

Movie- Do Aur Do PyaarProducer- ApplauseDirector- Shirsha Guha ThakurtaStarring- Vidya Balan, Prateek Gandhi, Sendhil, Ileana D'Cruz and othersPlatform – Cinema …

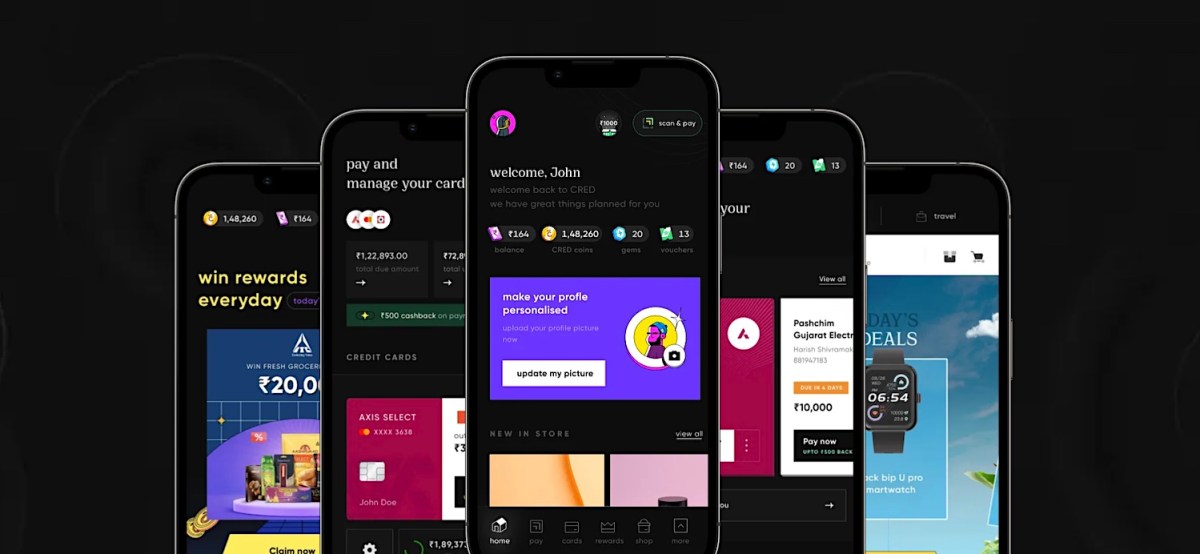

CRED has received the in-principle approval for payment aggregator license in a boost to the Indian fintech startup that could …

General Douglas MacArthur delivered his farewell address to Congress on this historic day, April 19, 1951, uttering the famous phrase: …

Taylor Swift shocked her fans early Friday morning by releasing a second half of her much-anticipated album “The Tortured Poets …

Ghoom Hai Kisike Pyaar Mein: The TRP rating of the serial 'Ghoom Hai Kisike Pyaar Mein' has dropped this week. …

THAT’S RIGHT. CHANDI. SO BACK ON MARCH 14TH, PENGUINS FANS CAME TO THE GAME EXCITED TO GET A JAROMIR JAGR …

Tensions flared in the House of Representatives Thursday when a group of conservatives confronted Speaker Mike Johnson, R-La., over his …

Generative AI models are increasingly being brought to healthcare settings — in some cases prematurely, perhaps. Early adopters believe that …